The new general secretary of Protermosolar is convinced that Concentrated Solar Power is the cornerstone to achieve the complete decarbonisation of the Spanish electricity system, by guaranteeing massive energy storage and providing firm and planned support for penetration with renewable intermittent sources like photovoltaic and wind energy. He also believes that if both the Government and companies comply with the PNIEC, Spain can once again lead the growth of solar thermal power in the world.

You came to the sector almost 15 years ago, when the start was given to the development of solar thermal in Spain. How did you live those moments?

They were really exciting moments and in my case I was not aware of the change that was coming. He worked as a fellow at Abengoa helping in the design of the PS10 tower but he could not imagine that companies such as Abengoa itself, Sener, Acciona, Cobra and many others would become world benchmarks in the sector, making the Spain brand the undisputed technological leader.

After this «splendor» stage, renewables were severely punished. How did the break affect the Spanish companies that were beginning to enter the solar thermal sector? Was the internationalization of Spanish companies one of its side effects?

Several factors converged. One was to reach the limit of solar thermal capacity to install that made new developments in Spain impossible. This fact forced companies to search for new markets. Many of the companies already had international experience; However, for almost all SMEs in the sector it was a milestone to establish themselves in countries such as the United States, South Africa, Chile or Morocco. Some of them were even installed with factories in those countries.

Additionally, the change in the remuneration scheme of the concentrating solar power plants that were already in operation occurred. This not only affected national plants, but we think that it had consequences beyond our borders in two aspects: the first is that many plans for solar thermal expansion by other governments were questioned when they saw what was happening in Spain. The second was the drastic change that forced many of our companies, which had a project promoter role, to become contractors for third parties. Although all this is very difficult to quantify, we believe that it contributed to a global slowdown in solar thermal power – precisely coinciding with a spectacular drop in the cost of photovoltaic energy – from which we began to emerge a few years ago with concentrated solar power-photovoltaic hybrid developments such as the from Dubai, demonstrating the complementarity of both technologies.

Now we have good times again. The PNIEC plans 5 new gigawatts for this CSP technology between now and 2030. Should we ask for more?

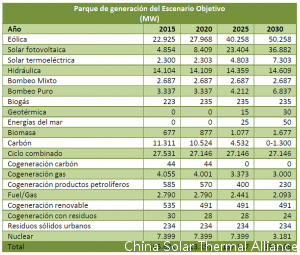

In Spain we have 2.3 GW installed, and that at the time was enough to demonstrate to the world that the technology was viable and that our companies were prepared to build reliable plants that a decade later continue to operate in a stable manner with highly predictable productions year after year. year. The 5 GW of new capacity foreseen by the PNIEC must be sufficient to demonstrate the importance of the solar thermal role in the new energy mix, which is none other than being the main – today almost the only – nightly renewable generation source that guarantees supply.

However, achieving full decarbonisation, planned for 2050 in the European Green Pact, does require more than 5 GW to guarantee a night supply without depending on fossil fuels. I would like to highlight that one of the PNIEC measures is aimed at increasing energy storage, which will help to have decarbonised strategic reserves to better match the generation and demand curves. In storage we distinguish between fast response storage services for frequency and voltage control and mass energy storage services – at a much lower cost – for their planned delivery to the system. We are in these second services, which are the calls to supply the night demand, reducing or eliminating the need for a fossil backup and therefore becoming the cornerstone to achieve complete decarbonisation of the electrical system.

Do you have the capacity to continue improving this technology?

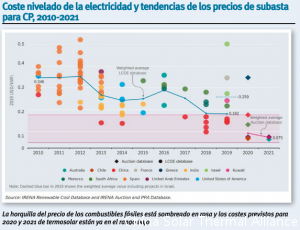

Completely. Not only with more storage, but also with larger turbine sizes that optimize cost, with a performance profile geared towards the evening / night and with the possibility of becoming that strategic reserve for peak demand, regardless of the previous days. They would have been sunny or not. Generation costs have been reduced, according to the International Renewable Energy Agency (IRENA) more than 47% between 2010 and 2019; and the prospects, based on the latest international auctions, foresee an even more drastic reduction of up to an additional 60% in the next two years. This allows, on the one hand, that in certain locations it is already more attractive to install a solar thermal power plant than one of fossil fuels and, on the other hand, as the solar thermal penetration in the energy mix increases, there is also a greater penetration of intermittent renewables since they have that firm and plannable support characteristic of our technology.

And in price? Is there room for it to continue falling and become fully competitive, not only with plants that use fossil fuels but with other renewables?

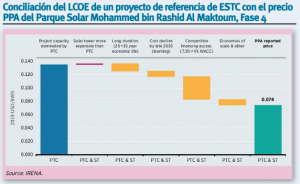

The price at which a solar thermal plant can sell its energy to be profitable does not depend solely on the «technological» costs, that is, on the investment in engineering, purchase of equipment, construction and labor necessary to operate the plant, but also of other external costs where the financial one stands out mainly. The plants planned to comply with the 5 GW of the PNIEC may involve an investment of more than € 25 billion, of which approximately three-quarters will be project debt with financial entities. Providing a stable remuneration framework in Spain is the key to keeping financial costs contained and not making energy more expensive. One of the main parameters that has allowed establishing the lowest solar thermal PPA to date has been precisely the reduction of the financial cost for the plants in Dubai.

How can solar thermal power now help rebuild the country, create jobs and wealth?

Solar thermal technology, as I have mentioned before, is eminently national. Not only at the engineering level, but also the construction companies and those that operate and maintain the plants. Furthermore, much of the supply chain is national. From Protermosolar we made a document of short-term proposals for economic recovery last April, in which we quantified that solar thermal can contribute more than € 1.3 billion of private investment and the creation of 5,500 jobs; 50 indefinite qualified jobs located in the Empty Spain and several thousand in the supply chain, only with the installation of molten salt tanks in some of the existing plants, reusing and maximizing the use of the rest of the infrastructure (turbine for electricity generation, connection point, etc).

This does not require new auctions and responds directly to the PNIEC measure to increase the energy storage capacity in the country. Furthermore, it would hardly cost the electrical system any longer, since if the useful life of the facilities is extended, this additional investment could be undertaken with a refinancing of the asset. Right now it cannot be done because the current regulatory framework does not allow it, but if it were modified, we know that there is a high interest in the sector to install storage in existing plants.

Regarding the auctions announced by the Government, should they be started and scheduled now? What do you expect from them?

The entire renewable sector, not just the solar thermal, is waiting for these auctions to be announced and for us to see the specific text that will govern them. Right now we have the PNIEC that establishes the national objectives until 2030 to comply with the European Green Pact, and the Law on Climate Change and Energy Transition is being processed where it does talk about the processes of competitive competition (auctions) but without entering the detail of its operation. In order to provide the stability that investors and funders need, we expect not only the first auction, but a calendar that allows developers to plan its development in the next few years, and that the auctions are clear enough to allow them to project future income from these investments.

Do you think that Spain can once again lead the growth of this technology in the world?

I believe that Spain can return to lead the world sector if we comply with the PNIEC. And by complying I mean everyone, government, but also companies. The government is leading the way, although these objectives still need to be specified in an assigned capacity calendar that also allows companies to plan their capacities. But, on the other hand, we are aware that the first plants to be redeveloped in Spain will mark the future from which they may come. If these first plants reflect the cost reductions that we have seen internationally, the financing entities manage to offer a low cost of debt and the lessons learned in operation and maintenance are applied correctly, we will certainly see spectacular growth in the sector.

Outside of Spain, we are closely monitoring developments in the United States, Morocco, South Africa, the United Arab Emirates and China. In Europe, the solar thermal sector does appear in the respective PNIECs of some countries such as Italy, Cyprus, Greece and the one that seems most advanced, Portugal, although with very limited capacities.

How much presence is there of Spanish companies in the solar thermal power plants that are built today in the world?

The Spanish company has been practically omnipresent in all the projects developed in the world until recently. Of the 6.3 GW installed worldwide, our companies have had a relevant role in the Spanish 2.3 GW, approximately half of the 1.7 GW in the US, in 1 GW in South Africa and Morocco, the 250 MW of Israel and other minor stakes in China and India. Although much of the knowledge remains Spanish, there are already major international Saudi or Chinese competitors with developments without a Spanish presence. We believe that when there are auctions in Spain, almost exclusively Spanish companies will attend, which guarantees not only the creation of wealth and employment in our country, but also the strengthening of the industrial fabric in order to continue competing in international projects.

What do you think of the hybridization of solar thermal technology with other renewables? Is this one of the possible ways of the future?

The complementary use of solar thermal with photovoltaic is the perfect tool that the sun can bring to the energy mix. Photovoltaic energy, with really low technological and financing costs, generated in Spain last year from 8:00 a.m. to 7:00 p.m. An alternative is needed for those 12-13 hours in the afternoon / night. Electric batteries are the solution for a fast-response storage service, but low-cost mass storage for planned overnight use must come from solar thermal technology.

The solar thermal plants of a decade ago were not designed for this, but were designed to generate at maximum power and store during the day and dispatch part of the night; but there are even plants that do not have storage today – although they could install it as I mentioned. For new auctions, the optimum is that the photovoltaic generates during the central hours of the day and the solar thermal from early in the afternoon until the following morning. This complementary use of solar thermal and photovoltaic is not a hybridization in itself, it can be done at the electrical system level.

With photovoltaic there are several possible hybridizations. For example to supply the self-consumption of the solar thermal plant during the day or directly for a combined production as seen in other international plants. It can also be hybridized with biomass in certain locations, where the power block is shared. Wind technology, having a more homogeneous generation profile throughout the day, does not present the opportunity for natural complementary nature of photovoltaics, where we also ensure that there is a good solar resource.

You have been almost three months as General Secretary of Protermosolar. Have you had time to focus on the goals you plan to pursue during your tenure? Or has the Covid-19 been too strong a brake?

Fortunately, the impact of the covid has been limited in the operation of the existing plants thanks to the protection measures taken by each of the companies. Therefore, my activity in Protermosolar has developed with a certain “normality”. I think we have all grown accustomed during confinement to hearing a baby in the background on teleconferences. Yes, the most institutional part of the association has been limited, since face-to-face meetings with relevant actors cannot be held. We hope that part will be remedied no later than the fourth quarter of this year. Regarding the other objectives of Protermosolar, it has been possible to progress satisfactorily. We have held a Board of Directors, our annual General Meeting and there have even been new members.

I am fully confident that Spain can once again become the world concentrated solar power benchmark, we have the national and European objective, the regulatory framework is being prepared, we have the companies and the knowledge, we just need that new starting pistol that I experienced as a fellow almost 15 years ago years.